Learning to Understand Debt vs. Equity Risk—The Hard Way

Recently, one of our deal guides received a call from the owner and CEO of a middle market B2B services and software business. After nearly four years of underperformance and covenant defaults, the business finally appeared to be turning a corner, delivering consecutive quarters of growth and profitability. Expecting a pat on the back, the CEO instead received a demand from his lender to be refinanced out.

He was confused—and, candidly, frustrated.

What he did not understand—and what many operators learn too late—is that debt investors are paid to avoid downside risk, while equity investors are paid to endure it.

Situation Overview

Nearly four years ago, the diligence advisory firm where one of our deal guides works diligenced this lower middle market B2B services and software business on behalf of a private credit fund. The credit fund ultimately funded a management buyout, enabling the young CEO to buy out the founder and take near-full ownership of the business.

At the time, the company was experiencing rapid growth—on pace to more than double revenue and expand EBITDA even faster. The lender provided a one-stop financing solution. Leverage appeared reasonable given the growth trajectory. While there was some customer concentration, key relationships were supported by multi-year managed services contracts, and diligence suggested that even the project-based component of the business would likely extend over multiple years with follow-on work opportunities expected.

In hindsight, the company’s end market was still benefiting from pandemic tailwinds that would not only normalize but overcorrect. That reversion and overcorrection began shortly after closing, pushing the company into covenant default almost immediately.

What followed was nearly four years of volatility. Performance deteriorated, visibility declined, and the company remained out of covenant compliance. It was a white-knuckle period for the CEO—and for the lender as well. Through it all, the lender remained unusually patient and supportive, likely recognizing the importance of management and key customer relationships.

Eventually, performance began to stabilize. Growth, profitability, and cash flow returned, and visibility improved. For the first time in years, the CEO felt a sense of relief.

Then came the refinancing request.

When Debt Starts Behaving Like Equity

Our deal guide reminded the CEO of a fundamental reality: he owned the business because the lender had provided the capital to fund the buyout—and in doing so, he had made a contractual commitment that the business would perform at a certain level.

That underwriting case and its accompanying contractual promise had been broken for years.

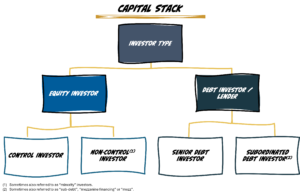

Debt and equity capital operate under fundamentally different risk frameworks:

- Debt investors are underwriting to consistency and downside protection.

- Equity investors are underwriting to long-term upside despite volatility.

For nearly four years, this lender was no longer taking traditional debt risk. They were effectively exposed to equity risk without equity upside.

At the original 10% blended interest rate—predicated on covenant compliance—the lender was being compensated for a stable credit. Even at a 12% default interest rate, they were not being compensated for the actual risk they bore. At the trough, enterprise value likely fell below the outstanding debt, meaning the lender was structurally impaired and underwater.

At that point, the nature of the risk had changed. This was no longer a credit defined by predictable cash flows and covenant protection. It was a credit dependent on enterprise value recovery.

In other words, the debt position was behaving more like equity.

While performance had improved, the business remained over-levered and out of covenant compliance. From the lender’s perspective, the recent progress did not reset the risk profile—it simply created an opportunity to exit the position.

There was no viable “debt-only” refinancing solution. Any solution would require new equity, and equity is inherently dilutive. It was only upon this revelation that the CEO began to understand the difference between debt and equity risk and the fact that the current lender had been—and was still taking on—more equity-like risk.

How the Situation Resolved

Ultimately, the CEO negotiated with the lender to remain in the credit for an additional eighteen months. However, that extension came at a cost: a higher interest rate, a tighter and less forgiving covenant package, and a meaningful equity component in the form of warrants.

A difficult outcome and lesson for the CEO owner—but not the worst-case scenario.

With a less patient lender, the result could have been far more severe, including a full loss of equity rather than partial dilution.

The Takeaway

The CEO came to understand—through experience—the difference between debt and equity risk.

The lesson is simple, but often misunderstood: lenders are not long-term partners in volatility; they are partners in predictability. When a business begins to behave unpredictably, debt capital often does not become more patient—it becomes uneasy and more transient.

In leveraged transactions, you do not get to unilaterally decide whether your capital structure behaves like debt or equity. The performance of the business and the various parties around the table have a say.

And once debt starts behaving like equity, expect the lender to want to be financed out or to be compensated for the risk they are bearing.