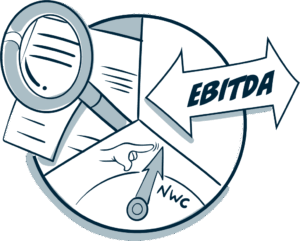

Net Working Capital (“NWC”) can influence valuation and purchase price in two fundamental ways. Many deal teams fixate on the second, more visible way (the closing adjustment), while under-appreciating the first (its impact on free cash flow). Both matter—often materially—so we break them down here.

1. NWC Impacts FCF.

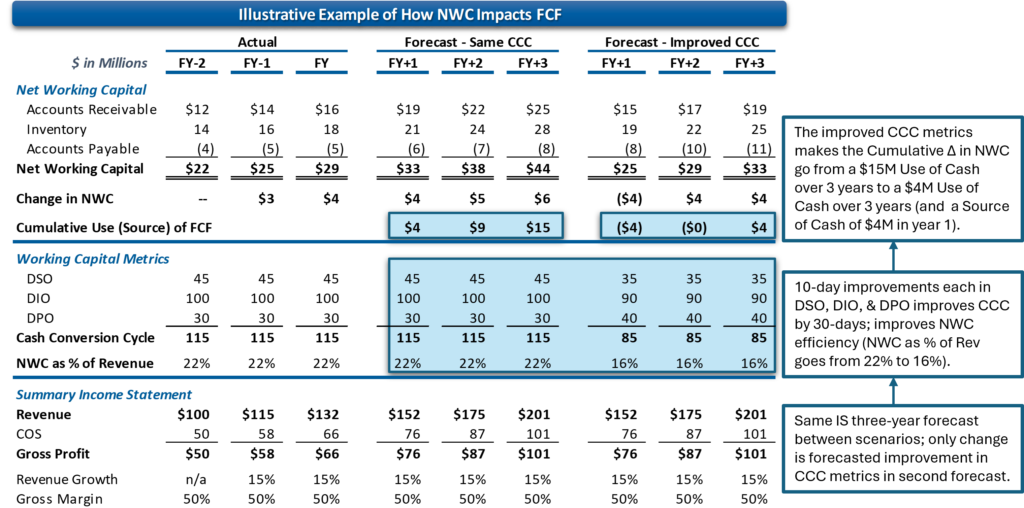

Changes in Net Working Capital directly affect Unlevered (Operational) Free Cash Flow (“FCF”). Because a business is valued based on the net present value (“NPV”) of its future cash flows, anything that increases or decreases the amount of working capital tied up in operations will flow through to valuation.

Consider a strategic buyer forecasting improved cash conversion metrics—faster receivables collection, quicker inventory turns, and more favorable vendor terms. These improvements shorten the cash conversion cycle, reducing the NWC investment required to support operations. Less cash tied up in NWC increases the forecasted FCF. Holding everything else constant, higher FCF translates into a higher valuation.

2. NWC as a Purchase Price Adjustment Mechanism.

Net Working Capital also plays a critical role as a common purchase price adjustment mechanism at closing. A “target” or “peg” NWC level is negotiated so the business transfers with a normal, sustainable amount of net working capital. Deviations from this target adjust the purchase price up or down. This mechanism protects both parties:

- Sellers should not benefit from delivering too little NWC (forcing the buyer to inject cash immediately post-close).

- Buyers should not receive a windfall from too much NWC being left in the business at close.

The purpose is fairness—the NWC adjustment does not change the intrinsic value of the business. Instead, it ensures the transacted price reflects whether the buyer is receiving more or less working capital than agreed upon (necessary because NWC can fluctuate seasonally or simply based on timing issues of large receivables or payables relative to the closing date). It also mitigates opportunistic behavior, such as sellers accelerating receivables, deferring needed inventory purchases, or stretching payables in the weeks leading up to close.

Bringing It Together: Why NWC Analysis & Normalization Matters

Just as the income statement requires scrutiny and normalization, the balance sheet deserves equal attention. Normalizing NWC serves two important functions:

- Understanding Ongoing Operating Needs. It provides insight into the NWC investment required for the business to operate in the ordinary course—information that directly impacts future FCF and valuation.

- Setting a “Fair” and Defensible NWC Target. It forms the basis for establishing a closing NWC target that avoids surprises, prevents gaming, and helps ensure a fair transaction (or positions you to negotiate an advantageous target).

Together, these analyses help deal teams arrive at more accurate valuations, avoid value leakage, forecast cash needs, and negotiate with clarity around one of the most frequently misunderstood components of M&A transactions.